US Economic Headwinds Intensify as New Federal Reserve Chair Focuses on Price Stability: Analyst Warns of Recession Risks and Rising Consumer Distress

WASHINGTON — U.S. economic signals are flashing warning lights as new Federal Reserve leadership prioritizes inflation control, while labor market data, consumer debt burdens and bankruptcy filings paint a picture of slowing growth and household strain.

In recent weeks, data on employment revisions, low labor force participation and surging personal and small-business bankruptcies have raised concerns among economists and market participants. Inflation has eased below the Fed’s 2% target in some measures, yet alternative gauges and persistent cost pressures suggest the situation remains delicate.

Federal Reserve Chairman Kevin Warsh, confirmed in May 2026 and now steering the central bank in the direction of his nomination, has emphasized data-driven decision-making and reduced reliance on frequent public statements. Markets have welcomed the shift, though analysts watch his upcoming congressional testimony closely for clues on policy direction.

Labor Market Strains Mount with Record Revisions and Participation Drop

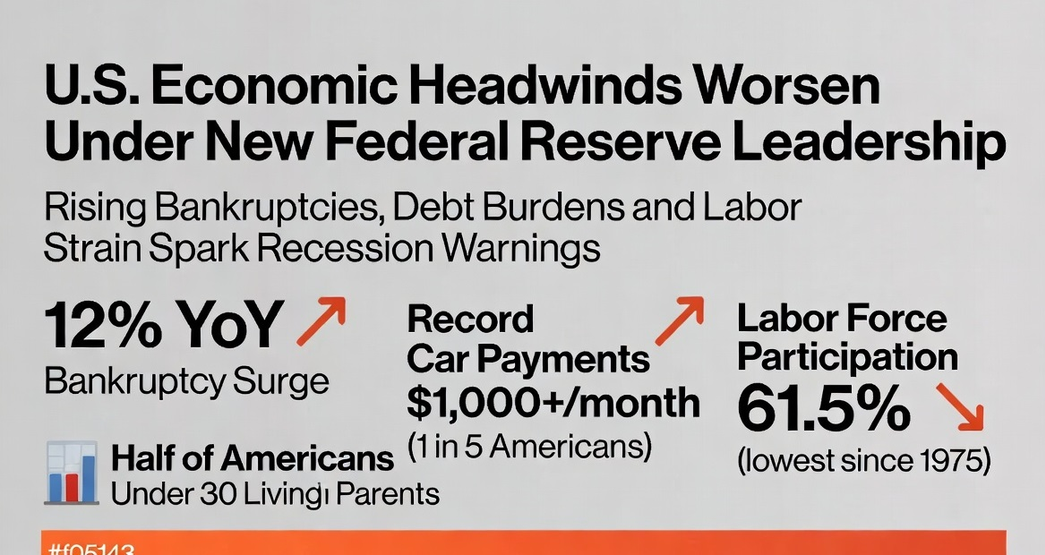

Payroll employment reports have undergone multiple downward revisions since the start of the year, undermining their reliability as a gauge of economic health. The latest June figures showed a modest gain of just 57,000 jobs — well below expectations and after prior cuts — while the labor force participation rate fell to 61.5%, the lowest level outside the COVID pandemic since 1975.

This decline reflects Americans opting out of the labor force, a trend linked in commentary to young adults delaying household formation. Census data indicate that more than half of Americans under age 30 now live with their parents, compared with a prior high of 60%. Such delays hinder the natural cycle of moving out, marrying and starting families — key drivers of economic activity and household spending.

The shifts are not abstract. They coincide with a sharp rise in consumer debt and reduced savings. The personal saving rate, which averages across all income levels, sits at historically low levels. Revolving credit has declined as lenders tighten standards, though this is partly offset by surging auto loans. One in five Americans now carries a car payment exceeding $1,000 monthly, contributing to auto delinquencies and broader credit stress.

Bankruptcy Filings Surge as Economic Pressures Mount

Bankruptcy filings across the board have climbed sharply in the first half of 2026. Total filings rose about 12% year-over-year to more than 310,000, with individual (household) bankruptcies up 12% and small-business Chapter 11 filings up 28%. Subchapter V elections for small businesses alone jumped 50%.

These numbers align with softening consumer sentiment and reflect the strain on households facing high fixed costs. The trend extends beyond small enterprises to corporate cost-cutting, including hiring freezes and layoffs — particularly visible in technology sectors such as Microsoft’s recent reductions.

Corporate and Household Stress Fuel Broader Economic Concerns

With record car payments and tight credit standards, many consumers have limited discretionary income. This dynamic is forcing companies to absorb higher input costs through layoffs rather than margin erosion. The result is a feedback loop: weaker purchasing power leads to further cost reductions, which in turn dampen spending and growth.

GDP forecasts remain subdued, with Atlanta Fed estimates around 2% for the current quarter when AI-related spending is stripped out. Inventory restocking — once viewed as a potential industrial renaissance — has peaked and is now winding down. Imports have surged in response to tariff policies and geopolitical developments, temporarily inflating GDP figures but raising questions about sustainability.

Alternative Data and “Real-Time” Inflation Measures Gain Attention

Traditional measures have shown inflation easing, with one daily price gauge at 1.9% year-over-year. Yet officials have signaled openness to alternative metrics, including trimmed-mean calculations that exclude volatile components.

The Fed has established a task force to explore such real-time data sources. Should these prove more reliable in signaling economic conditions, they could reshape how policymakers interpret the outlook — potentially influencing bond yields, borrowing costs and household decision-making.

No Official Recession Declaration Amid Public Job Losses

The National Bureau of Economic Research’s traditional recession criteria — two consecutive quarters of shrinking GDP or equivalent indicators — have not yet been triggered on a net-job-loss basis in recent quarters. However, critics argue that repeated payroll revisions and net employment declines in prior periods warrant closer scrutiny. The NBER has not commented publicly, and the Fed has avoided framing its actions under a formal recession declaration.

Balance-sheet expansion continues, but not explicitly tied to a recession call. Whether and when the NBER will recognize a downturn remains a point of debate, with political timing around midterms adding another layer of complexity.

Outlook for Interest Rates and Gold as Hedge

Interest-rate expectations have shifted with the new leadership. Markets anticipate possible easing to support growth, though the focus remains on achieving and maintaining price stability. Inflation expectations have moderated with lower energy prices, but the path ahead depends on labor market resilience and alternative inflation readings.

Gold, which has consolidated after an earlier sell-off, is viewed by some analysts as offering a potential entry point amid rising uncertainties in credit markets and higher government borrowing costs. Bond yields have edged higher, increasing interest expenses for the federal government — already exceeding $1 trillion annually — and pressuring mortgage rates and housing affordability.

Purchase mortgage applications remain flat year-over-year, but rejection rates exceed 40%, limiting buyer pools. Price declines are reported in some markets, though inventory is beginning to restock.

Federal Reserve’s Data-Dependent Path and Market Implications

The new chairman’s approach — reducing excessive Fed speak and letting data speak — is broadly welcomed by investors. However, success will depend on the resilience of the labor market, the staying power of disinflation and the economy’s ability to absorb higher debt-service costs without tipping into contraction.

For now, economic data continue to align on downside risks: slower hiring, elevated debt burdens, delayed household formation and rising corporate stress. Policymakers, investors and households are watching closely for the next set of employment reports, inflation prints and congressional testimony to assess whether the current trajectory signals a broader slowdown or manageable adjustment.

Analysts at firms such as Qi Research continue to track these developments, emphasizing the need to understand underlying flows, credit cycles and alternative data indicators rather than relying solely on headline statistics.

As the Federal Reserve navigates its new era of data focus, the coming months will test whether the institution can modernize its toolkit while steering the economy through a period of heightened vulnerability.

{kind=link}